Debts Management: efficient strategies to get out of the red and regain your financial health

Learn how to identify, organize and renegotiate your debts, using practical strategies to eliminate them and take the first step towards a stable, worry-free financial life.

Reviewing the previous step

If you've been following our series, you already know how important it is to have a good credit score to open doors in the financial market. However, for those who have accumulated debts, improving their credit can seem like a distant challenge. The good news is that getting out of the red and recovering your financial health is entirely possible with the right planning.

In this post, we'll present practical and efficient strategies for organizing your debts, learning how to renegotiate them and establishing a realistic plan to get rid of them once and for all. Are you ready to take the first step towards a lighter financial life?

Getting to the point...

Managing debt can seem like an impossible task, but with the right strategies and a good plan, you can turn the tables and regain your financial peace of mind. In this post, we'll show you 5 essential steps to organize your debts, choose the best payment method (such as avalanche or snowball) and achieve your financial freedom.

Shall we go together?

Managing your debts in 5 steps

Step 1: Identify all your debts

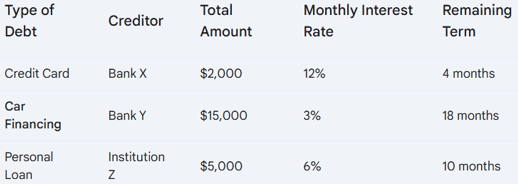

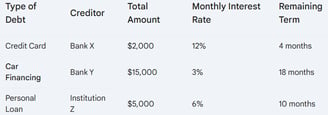

The first step to solving any problem is to know the situation in full. List all your debts, including:

Total amount of debt.

Creditor (bank, card, financing).

Interest rate.

Payment period.

With this detailed overview, you can prioritize the most expensive debts and create an action plan.

Step 2: Prioritize high-interest debts

High-interest debts grow quickly and can get out of control. Prioritize paying off these debts first.

Credit card and overdraft debts usually have the highest interest rates.

Then focus on financing and loans with lower interest rates.

Practical strategy: If possible, use a partial emergency reserve or extra income to pay off small, high-interest debts. This relieves the budget and reduces stress.

Step 3: Renegotiate your debts

Negotiating with creditors can be a great solution for reducing the total amount owed and making it easier to pay. Many institutions offer

Installments with lower interest rates.

Discounts for paying in full.

Extended deadlines to suit your possibilities.

Practical tip: Take advantage of renegotiation fairs, such as those offered by Experian, which facilitate agreements between debtors and creditors.

Step 4: Adopt the Snowball or Avalanche strategy

There are two main strategies for eliminating debt efficiently:

The Snowball method:

Pay off the smallest debts first.

When you pay off one debt, use the amount for the next smallest.

Advantage: The feeling of fast progress helps maintain motivation.

Avalanche method:

Prioritize debts with the highest interest rates.

Reduce the total amount you spend on interest over time.

Practical example: If you have a debt of $2,000 (12% interest) and another of $5,000 (6% interest), using the avalanche method, pay off the $2,000 debt first.

Step 5: Create a realistic budget to pay off debts

If you've followed our previous posts, you know how to set up a family budget. Now, use this tool to include your debts:

Set aside a fixed percentage of your income to pay off debts.

Identify where to cut unnecessary spending.

Direct any extra income to accelerate payments.

Example: If you earn R$3,000 a month, set aside 20% (R$600) to pay off debts and negotiate terms that fit this amount.

Extra tips to get out of the red faster

Avoid taking on new debts while still paying off old ones.

Use your thirteenth salary or bonus to pay off debts.

Increase your income with temporary or freelance work.

Conclusion

Resolving your debts is more than an obligation; it's a fundamental step towards regaining your financial peace of mind and paving the way for new achievements. With organization, negotiation and discipline, you can transform your financial situation efficiently.

Want to know more? Click on the button below to access the next post!

To access the other InvestZone's posts, click on the button below!

In the next post, we'll talk about Credit Cards: find out how to use your card wisely, avoid abusive interest rates and even turn it into a tool for generating extra income. Don't miss it! 🚀

For investors who have just arrived, this is the first post in our second series of articles on Debt Management and Emergency Reserves.

So, did you like the tips? Share your experiences and questions in the comments!

Share your experience with us! If you have any questions, want to know more about debt management or simply want to talk about it, feel free to leave a comment! And don't forget to check out our blog for more tips and information on finance!

What's your opinion?

Investments

We help you control your personal finances and invest safely and effectively.

Income

suporte.investzone@gmail.com

© 2024. All rights reserved.

Comments section